Risk Arbitrage

Alternative investment strategies: RiskArb.

Andrea Leporati

CEO

Historical origins

Risk arbitrage, often termed merger arbitrage, has its roots in mid-20th-century Wall Street, where only a handful of brokerage firms discreetly exploited pricing inefficiencies surrounding announced mergers. Originally practiced within the proprietary trading desks of investment banks, it remained a niche, opaque activity. The strategy’s institutionalization began in the 1970s, as regulatory reforms and the liberalization of capital markets allowed independent partnerships and later hedge funds to specialize in event-driven strategies. By the post-2008 era, after the Volcker Rule restricted banks from proprietary trading, risk arbitrage had migrated almost entirely to hedge funds and multi-strategy platforms. The strategy’s evolution from a niche “back-office secret” to a data-driven, quantitative discipline reflects the broader transformation of financial markets themselves. As access to information improved through regulatory disclosures, technological advances, and global capital mobility, merger arbitrage shifted from opportunistic speculation to a systematic investment approach grounded in empirical analysis and risk management.

2. Theoretical structure of the strategy

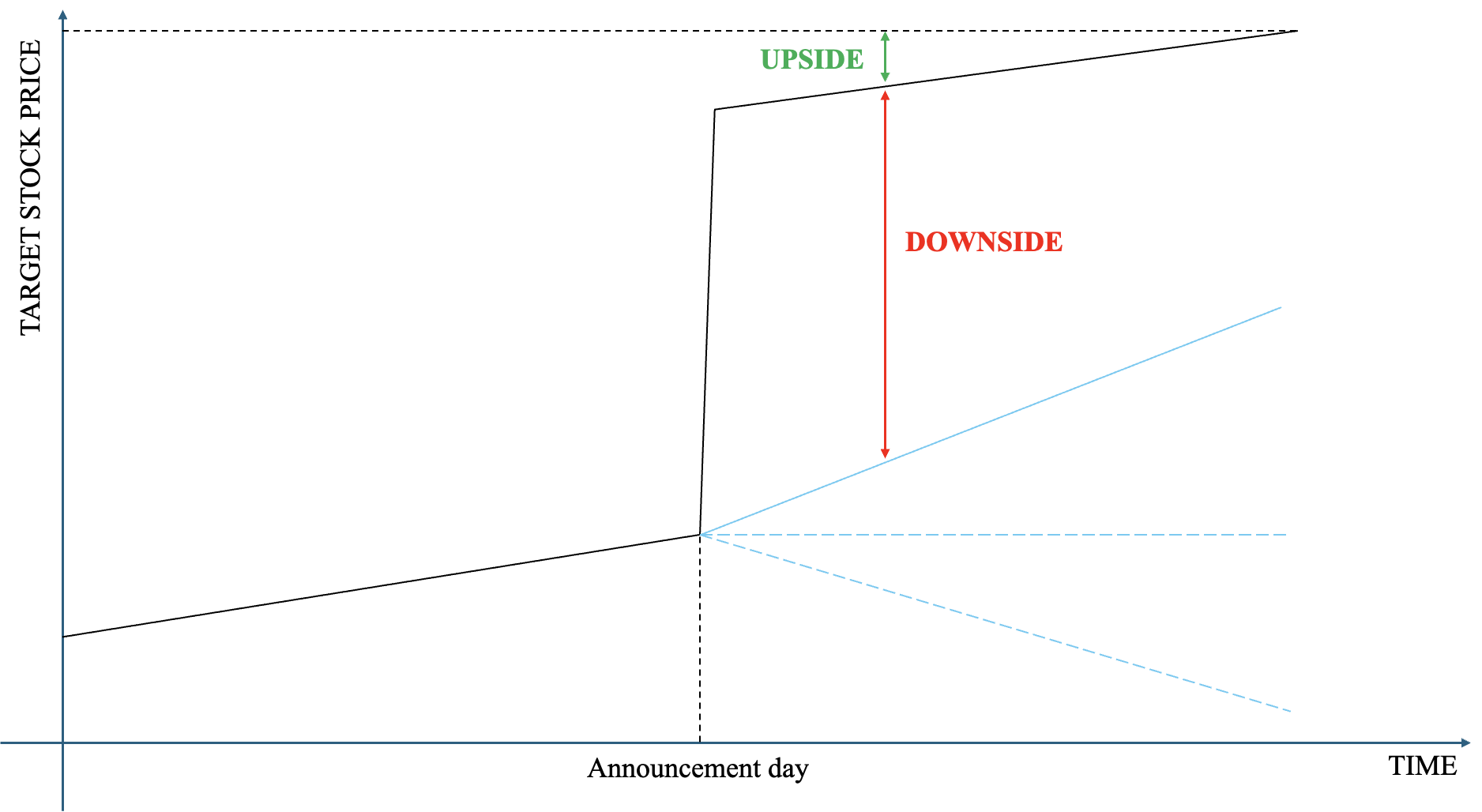

At its core, risk arbitrage exploits the temporary mispricing between a target’s market price and the value implied by an announced acquisition offer. Once a merger or tender offer is made public (Announcement day), the target’s share price typically rises toward, but remains below, the offer price, reflecting the residual probability that the transaction may fail. The arbitrageur’s task is to estimate the likelihood of completion and to capture the spread conditional on success. Unlike classical arbitrage, which locks in riskless profit through simultaneous offsetting trades, merger arbitrage requires probabilistic reasoning under uncertainty. The payoff structure is asymmetric: limited upside upon deal completion and potentially significant downside if the merger collapses. In the graph below the distance between the current market price and the offer price defines the upside, and the gap to the estimated break price defines the downside. The spread compensates investors for bearing legal, regulatory, and financing risk, and, under equilibrium conditions, it converges toward zero as deal closure becomes imminent. The deal valuation depends on two central parameters: the spread conditional on success and the implied “even-money” probability at which expected value is neutral. This structure enables arbitrageurs to treat each deal as a binary contingent claim and to aggregate multiple positions within a probabilistic portfolio framework. Because deal outcomes are largely idiosyncratic, driven by regulatory, contractual, or corporate-specific factors, correlations between positions are close to zero, granting risk arbitrage portfolios valuable diversification properties. Yet, systemic shocks, clustered deal failures, or liquidity contractions can momentarily invalidate independence assumptions. Hence, modern risk arbitrage relies on dynamic optimization and constant recalibration of position sizing to maintain equilibrium between expected return and conditional risk exposure.

3. Formulas at the basis of the strategy

At its foundation, risk arbitrage seeks to exploit the temporary mispricing between the market price of the target’s shares and the offer price S proposed by the acquirer. When a merger or tender offer is announced, the target’s stock price typically jumps but remains below S; the expected stock value if the deal fails denotes the break price B. The arbitrage spread, or upside, is given by: and the potential downside, conditional on failure, by .

We can further define the even-money probability as the probability that makes the expected payoff of the deal equal to zero:

Rearranging, we discover that the market price today reflects the expected value of the deal:

4. Case Study: The LVMH–Tiffany & Co. Merger

The acquisition of Tiffany & Co. (target) by LVMH (acquirer) illustrates how risk arbitrage involves not only financial valuation but also the interaction of legal strategy, macroeconomic shocks, and investor behavior. Initially viewed as a near-certain transaction, the deal’s spread widened sharply in 2020 as the pandemic disrupted global luxury markets and LVMH sought to withdraw, citing material adverse effect clauses and diplomatic tensions. The subsequent litigation in Delaware reshaped market expectations of deal completion, transforming what had been a narrow spread into a substantially wider one. The eventual renegotiation, resulting in a modestly reduced offer and successful closing, demonstrated that merger arbitrage returns are driven not by static price discrepancies but by the continuous reassessment of probabilities, information asymmetries, and market sentiment by arbitrageurs.

5. Contemporary relevance

In contemporary markets, risk arbitrage represents a refined intersection of law, finance, and data science. The strategy’s intellectual appeal lies in its synthesis of quantitative modeling with qualitative judgment, assessing antitrust probabilities, shareholder behavior, and geopolitical context within a probabilistic framework. Advances in computational finance have enabled more precise estimation of implicit success probabilities, while increasing regulatory transparency has enhanced data availability. Nonetheless, success in risk arbitrage remains as much about interpretation as calculation: it requires the disciplined skepticism to question market consensus and the flexibility to adapt as deal narratives evolve. As global M&A activity continues to expand and diversify, risk arbitrage stands as a paradigm of applied financial reasoning, an enduring example of how uncertainty, properly structured, can itself become an investable asset.